Simon Harris has ignited a debate about saving in Ireland in the last few weeks, contending that “too much of people’s hard-earned savings remains in low-yield deposits, where inflation can erode value over time.” He’s not totally wrong, in fairness to him – of the €171 billion (January 2026, Central Bank) in Irish deposit accounts (according to the Central Bank), it is unlikely any are making any kind of return in savings interest. That’s internationally unusual – in Germany, the average rate of return on savings is north of 2%, in the United States, it’s up to 5%. There is a real question as to why Irish savers are treated differently and why our banking system seems to give so little value for money as opposed to other jurisdictions.

Of course, as is too often the case in Irish political debate, that question has also been intermingled with tax treatment on returns. In Ireland, our treatment of returns on savings is dictated by a DIRT tax – a 33% tax at source on savings interest. However, if you were to say that savings should also include investments – money paid into an investment account that might then be invested in equities (shares in companies), bonds, and other financial instruments – then you might also look at two other tax dynamics: capital gains tax (CGT) and deemed disposal.

Capital gains taxes are a feature of taxes in other jurisdictions, too. Effectively, they’re a tax on the gain in the value of the underlying investment (or asset) over time. In some countries, like the US, there are more complex regimes – taxes that differentiate on how long you’ve held the investment, for example (short-term CGT at ~40% and long-term capital gains at 20%), or what kind of asset it is (property vs. options in a company’s shares vs. actually holding the shares), or how that compares to your overall tax paid (minimum effective tax rates and alternative taxes). In Ireland, we have a straight CGT of 33%.1 We also do something a bit different from other jurisdictions in that we apply CGT every 8 years, called ‘deemed disposal’ – meaning you become liable for the tax, even if you haven’t actually collected the return, every 8 years.

1Post-publishing note: A capital gain tax on exchange-traded funds (ETFs) is called an ‘exit tax’ in Ireland – the tax rate is dependent on where the ETF is domiciled, but Irish-domiciled ETFs see an exit tax at 38% for as of 1 January 2026. For the purposes of illustration in this post, I refer to the CGT and exit tax interchangeably and apply a 33% rate.

Personal finance advocates have compared our tax treatment to other jurisdictions and gotten more vocal in recent times, at the disparities in our tax systems vs. our international counterparts. They claim the tax treatment on CGT being higher, with fewer exemptions, and this deemed disposal dynamic is unfair vs. how it’s treated in other countries. Throw in the fact that many younger people are accumulating savings with little return, and yet still find themselves locked out of their desired properties vs. older generations, and that perceived injustice feels a bit more acute. I get that.

Who Are We Talking About Here?

It’s worth taking a step back and actually looking at the data here: how much are we talking about and how would it affect different people? Well, helpfully, the central bank (via the ECB) breaks that information down – a measure of cash deposits in the Irish banking system on a ‘net wealth’ per capita basis:

| Q3 2025 | Total | Household | Per Capita | |

| Quintile 1 | Bottom 20% | €5.33B | €13,890 | €5,570 |

| Quintile 2 | Bottom 20% to Bottom 40% | €18.39B | €47,960 | €18,900 |

| Quintile 3 | Bottom 40% to Top 40% | €20.71B | €53,980 | €20,600 |

| Quintile 4 | Top 40% to Top 20% | €37.8B | €98,570 | €37,050 |

| Quintile 5 | Top 20% | €110.02B | €286,540 | €100,300 |

If you look at the top deciles, you’ll see that the top 20% of deposit holders hold the majority of savings in the State:

And if you look at households, you’ll see the top 10% of households have a whopping 40.61% of all savings in net wealth on deposit in Ireland. Some people have done very well from Ireland’s economic recovery, and it’s fair to say not everyone has done.

Why Savings Returns and Investments Matter from a Public Policy Perspective

So why does how people save and invest matter? Well there’s a few issues at play. In the first instance, individuals want to make their hard-earned savings work for them in the same way as a pension does: creating longer-term financial security. That’s fair enough on one level. There are, however, a lot of other reasons for policy-makers to be interested in how savings are deployed in the Irish banking system and the wider societal effects.

First of all, how people save and invest is directly related to how much the State needs to do to help people age with dignity. If people on lower incomes, for example, don’t save or invest in their pensions, then later on the taxpayer will have to pick up the tab for their survival after their working life through higher State pensions. That was a key argument for the implementation of the Autoenrolment scheme launched this year – a State mandate that every PAYE worker after €20,000 in income would have to save into the My Future Fund or their occupational pension. Importantly, while it’s framed as a ‘pensions measure’, it’s actually a savings and investment scheme run by investment managers on behalf of the State with State and employer contributions, yielding a lump sum payment to the individual at the end of their working life based on the returns from investment.

Secondly, investments are a key part of how the modern world creates economic activity. In simple terms, banks use savings to then provide loans to other people. In classical banking, these loans are supposed to be used to provide credit to individuals and businesses to generate economic activity. Of course, the loan people are most familiar with is a mortgage, but loans can also include things like start up loans to businesses. In the last century or so, instead of direct loans, banks also invest the money in other things (like the stock market) to generate returns. The difference between the returns they get from those investments and the returns they give to savers, in simple terms, is the profit for the bank. In Ireland, since virtually no returns are given on savings, banks take all that return for themselves, paying out to their shareholders in dividend payments. That in itself is unusual when you compare it to what happens internationally.

But more to the point, the banking system – also known as financial intermediaries – in providing credit to individuals and businesses, is supposed to be the lifeblood of economic prosperity. Without those loans (or credit more widely defined), businesses don’t start, they don’t expand and hire more people, they don’t invest in developing new products and services. Fundamentally, we need those things for economies to function in the modern world – and this has been the case since about the 1600s with the advent of capitalism. As a social democrat, I’d prefer more interventionist policies towards socialist running of the economy, but I recognise that in practical terms we live in a capitalist economy and I see my job as making sure it’s tempered so that the vulnerable are protected and that prosperity is shared as widely as possible. How we manage banking, savings, and investments, is a core part of that.

Importantly, how banks or other financial institutions lend money can have significant social benefits. The Social Democrats proposed a ‘Homes for Ireland Savings Account’ to turbo-charge homebuilding in Ireland, for example – a really important and potentially transformative proposal. Why would we just let €171 billion in deposits sit in bank accounts while we have a real deficit in indigenous financing for homebuilding? Why would we allow that and force big developers to go to international capital markets and private equity, with much higher loan interest rates, that force up the cost of housing and property prices? It would be a much better use of our resources to make saving, investing, and building a national effort we can all be a part of, and it’s a policy proposal I’m really excited to support.

Of course, homebuilding isn’t the only thing you can use savings to fund: infrastructure, renewable energy, capital development of public buildings like schools, etc. could all be targeted with the right State-led policies. Unfortunately, this government and previous governments have lacked any vision to do something like that, something we in the Social Democrats would like to see change. As I used to say to people on the doors when they asked me for the difference between the Greens and us, I’d say “Well, we both want to build offshore wind farms – they want private investors to own them, I want you to own them”. There is a real opportunity in public building and public capacity if we have the leadership and vision to do it.

There are 2 other issues that we have to be aware of as policy-makers, as well, in how savings are deployed. For one, there are systemic banking risks to how banks deploy their funds. That’s carefully managed by the Central Bank, but if, say, all those deposits were to en masse withdraw their savings and move to a new investment product independent of the Irish banking system, say on Revolut or E-trade, well you’d see the financial position of the Irish banking system rapidly deteriorate. This dynamic, known as a ‘bank run’, is an existential risk to any economy, something we haven’t seen in Western Europe in many decades, and one we must critically avoid.

The other issue that’s often not talked about is the question of where investments with savings are made. A few years ago, I was listening to a podcast from Ezra Klein, where he described how African American communities were saving in their local banks, and instead of those banks providing loans to the local community, they were using the savings to provide loans to adjacent white communities. There was a perceived lower risk and higher return in white communities, so the banking managers thought it was a better way of generating secure returns for their savers. The effect of that was that Black communities, despite saving, were deprived of their own capital or credit or loans to build or sustain businesses and community projects. The direction of the loan actually made the local community poorer, not richer, despite savings. The structural racism this represents is specific to this case, but you could apply the same dynamic to Irish (and European) investors who predominantly choose to invest in US or other foreign financial instruments – the capital effectively flows out of your economy, deprives it of credit, and makes your economy less prosperous. China has famously restricted this kind of capital flow and has seen major domestic investment booms as a result (among other reasons).

Okay, so by now we might have come to the conclusion that how we treat savings and investment matters, and there’s a real question in Ireland about how we should do that well. What are the other things we should consider?

What Are the Risks in Supercharging Returns for Savers?

Well in the management of any economy, we need to ensure investments are socially beneficial. Most of us would agree that investing in weapons, arms manufacturing, tobacco, etc. isn’t a good thing. Most pension funds avoid that for this reason. But there are others that aren’t avoided: fossil fuel companies worsening the climate crisis, companies with track records of human rights violations, or companies that engage in unethical behaviour on a variety of fronts like trade union crackdowns or bribery in developing economies. Being thoughtful about where our money goes is really important and managing that risk is key.

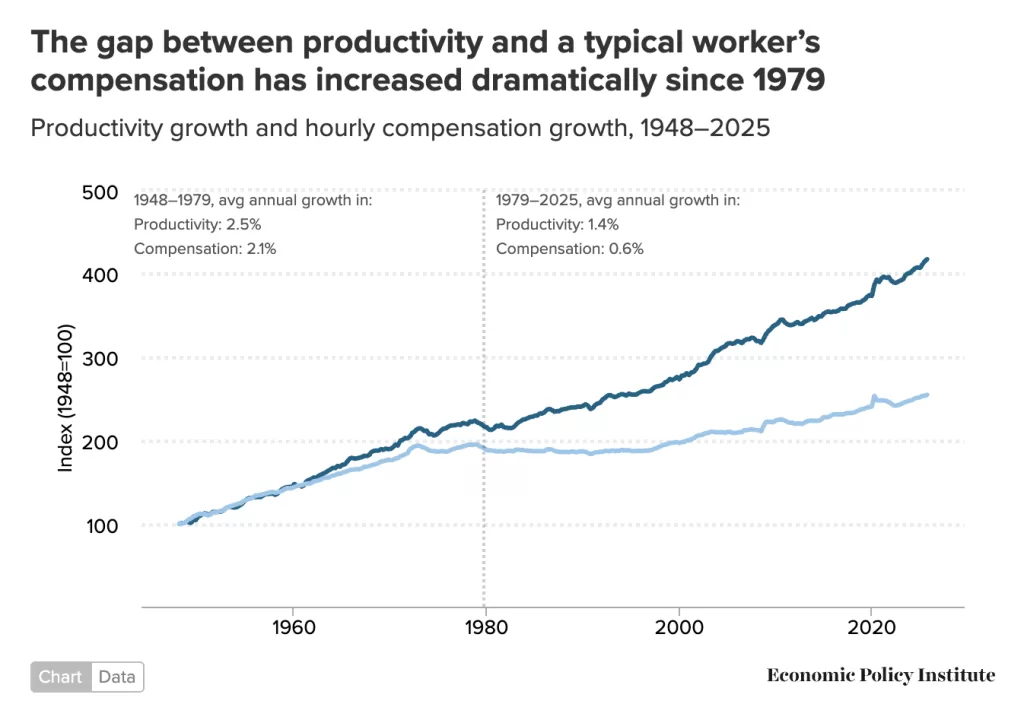

In a wider context, I think most people would appreciate that the world has gotten more unequal. I think of the following graph pretty often – the widening of the productivity gap in the US since 1979 where the fruits of capitalism have not gone to workers.

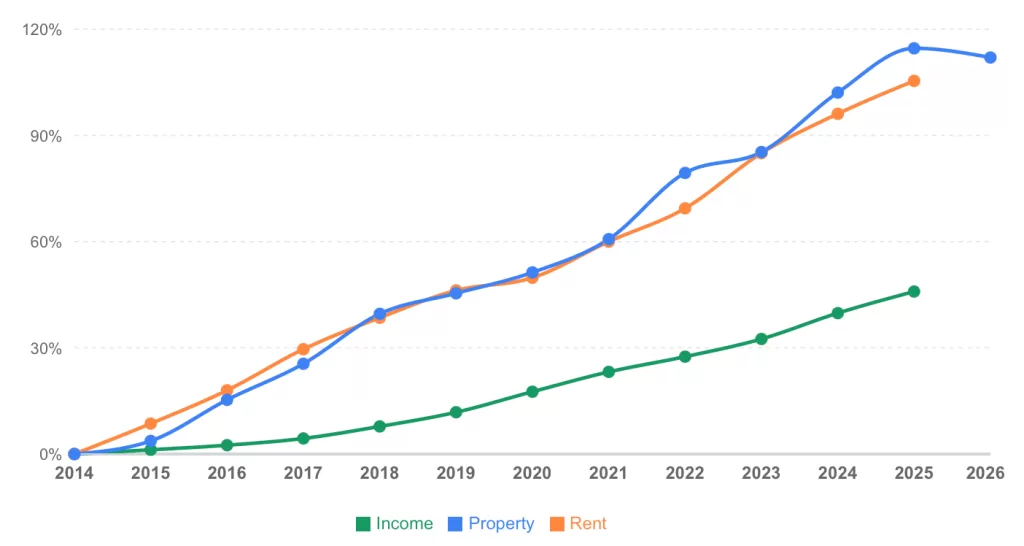

A similar and more recent graph exists on rents vs. income in Ireland (and that blog makes for some harrowing reading):

While we’re doing better in Europe vs. the US on labour gains, thanks largely to better workers rights protections and stronger trade unions, I think we’d all like to see a more equal world. Making sure that a savings and investment scheme corrects inequality and inequity instead of extending it is a worthy goal, in my view, and should be part of the conversation. Tax treatment, say, for the wealthy with large investment capacity vs. the poor with very little, is an important component of that.

There’s also the question of what should ‘pay’ in a society – working or investing. If your returns are higher in passive investing and the tax rate is lower than actually going out to work, that creates pretty perverse incentives and additionally creates a penalty for those that are predominantly reliant on their occupational income for a living. It should be lost on no one that the 33% tax on capital gains vs. the 40% marginal tax (plus USC, etc.) on higher-income work in Ireland is a differential that gives high net worth investors a leg up at the expense of someone who works to earn a crust every day. Progressive tax treatment matters, especially to social democrats and leftists like me.

More to the point, as a friend of mine pointed out to me recently, most investing isn’t aimed at generating credit for businesses or public projects. When someone trades on the stock market, they’re participating in what’s known as a ‘secondary market’, not investing their money in anything and they’re just trading between investors to try and buy low from one to sell high to another at a later date. Secondary markets are, in effect, a sophisticated form of gambling on the future value of an investment. That doesn’t really have any social dividend for anyone other than the person who got it right on where the value of the asset was going (although there is a minor, unconvincing, argument that secondary markets prove the value and liquidity of a company’s ability to raise capital).

One of the core risks that has emerged recently is that with the advent of social media, investment strategies and ‘finfluencers’ (or financial influencers) have become more commonplace and influential. The ‘investment bro’ caricature is very real, and often very misleading. Recently, the Money and Budgeting Service reported at the Oireachtas Social Protection committee that it was an emerging issue for financial security in at-risk populations and they and I had a bit of an exchange about that recently.

That is to say something that should be really obvious to anyone making any investment whatsoever: there is always a risk that you lose money. There’s even a risk you lose all your money (hello Eircom). That’s not said often enough about any kind of financial transaction – and, given how financial markets have performed in our lifetimes, people often expect they should lose no money no matter what they do or what happens. That was a key issue amidst the calls to “burn the bondholders” during the recession. Importantly, when you deposit cash in a bank in Ireland, it’s guaranteed under a European insurance scheme up to €100,000 (in the US it’s $250,000), but that’s a relatively new invention in Ireland. It’s worth noting that anything after that amount is not insured if the bank collapses, for those of you in the top 10% of Irish depositors.

And lastly, there’s the question of net wealth vs. gross wealth. If someone has €1,000 to invest, but doesn’t own a home yet, they’re in a different category to someone with the same amount but who owns their home outright. Someone who has only 5% of their mortgage paid off vs. the person who has 95% paid off is a different category again. We don’t often talk about this dynamic that much in Ireland, but net wealth taxation proposals like the one the Social Democrats have put forward really matter, and gross wealth taxation like property tax also matter too. Getting the right balance is important.

So What Does Simon Say?

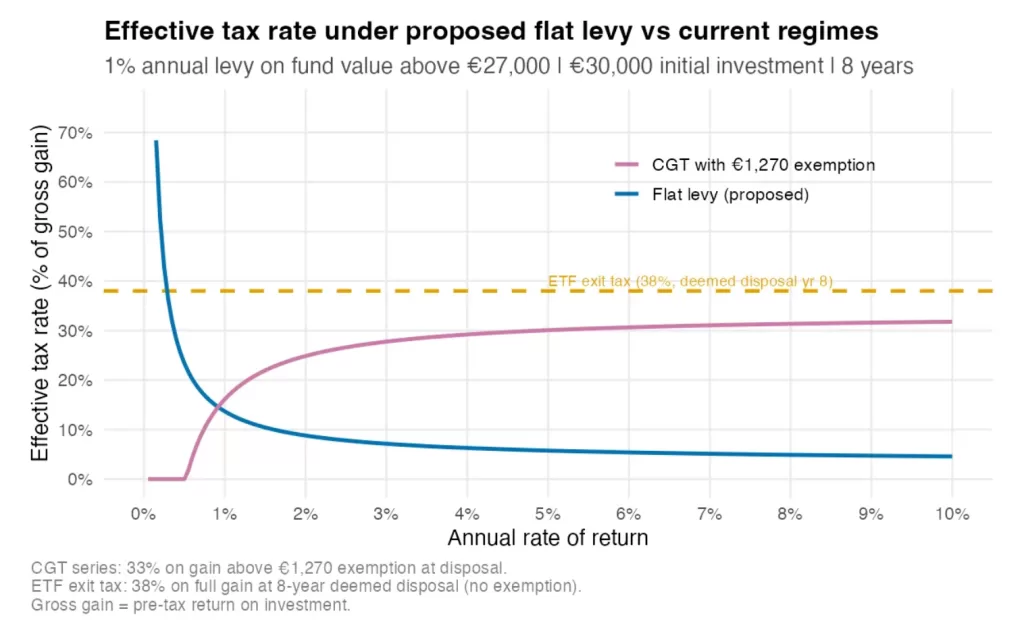

Which brings me to Simon Harris’s draft proposal, based on the Swedish ‘ISK’ scheme. In this scheme, people are taxed on their gross wealth in the investment account at a rate of about 1% and capital gains (and losses) are exempt from tax treatment. Let’s evaluate that for a second.

From a personal investor perspective, there’s a catch in this that Mr. Harris hasn’t emphasised: unlike today, where if you lost money on an investment, you’re not liable for any tax, in his propsals you would now be liable for a tax. So let’s say you invested that €1000. If it goes up by 5% to €1050, you now owe €10.50 in tax vs. the €16.50 you might have under the current regime. Happy days for you, right? Well yes, but alternatively if that investment lost 5%, then you’re left with €950 and you’re liable for a €9.50 tax vs. the €0 you might have under the current regime. So it’s not all net positive from a personal investment perspective.

From a left-wing perspective, it’s good to see a gross wealth tax being proposed and supported by the government. That’s not necessarily how most places do it, for example in the US. However, it’s worth pointing out, as did my colleague Cian O’Callaghan and the economist Barra Rowantree, that for much wealthier people who have diversified investments that typically generate net returns every year, this will likely mean a net wealth tax cut:

Someone who invested €1 million euro across a myriad of different assets is likely to get a return of about 10% per year. Instead of being liable for that €33,333 in capital gains, they’re likely to only pay €13,333. At scale, that is likely to have a significant impact on the fiscal position of the State, in an age where most economists are calling for a more diversified tax base, not less. If the scheme allows high net worth investors to cut their taxes, and wealth taxes for the State to go down, then that’s almost certainly a bad thing.

Conclusion

For my part, I think any new savings and investment scheme has to pass a few tests:

(a) is it supporting long-term financial security for the Irish population?

(b) is it focused on creating socially-good outcomes?

(c) is it reducing a comprehensive view of socio-economic inequality in our society instead of widening it?

(d) and is it supporting our indigenous economy so we can build the infrastructure, goods, services, and businesses of the future?

I don’t think that Harris’s proposal hits the mark on all of that. There’s also probably a good bit more to be fleshed out in terms of progressive taxation for larger quantums of investing and how we restrict the use of funds to socially-good investments and supporting developing the Irish economy, in particular. But I’m hopeful we might be at least starting the right conversation – for Irish savers and for our shared economic prosperity.